Why Insurance Companies Delay Settlements After Medical Examinations

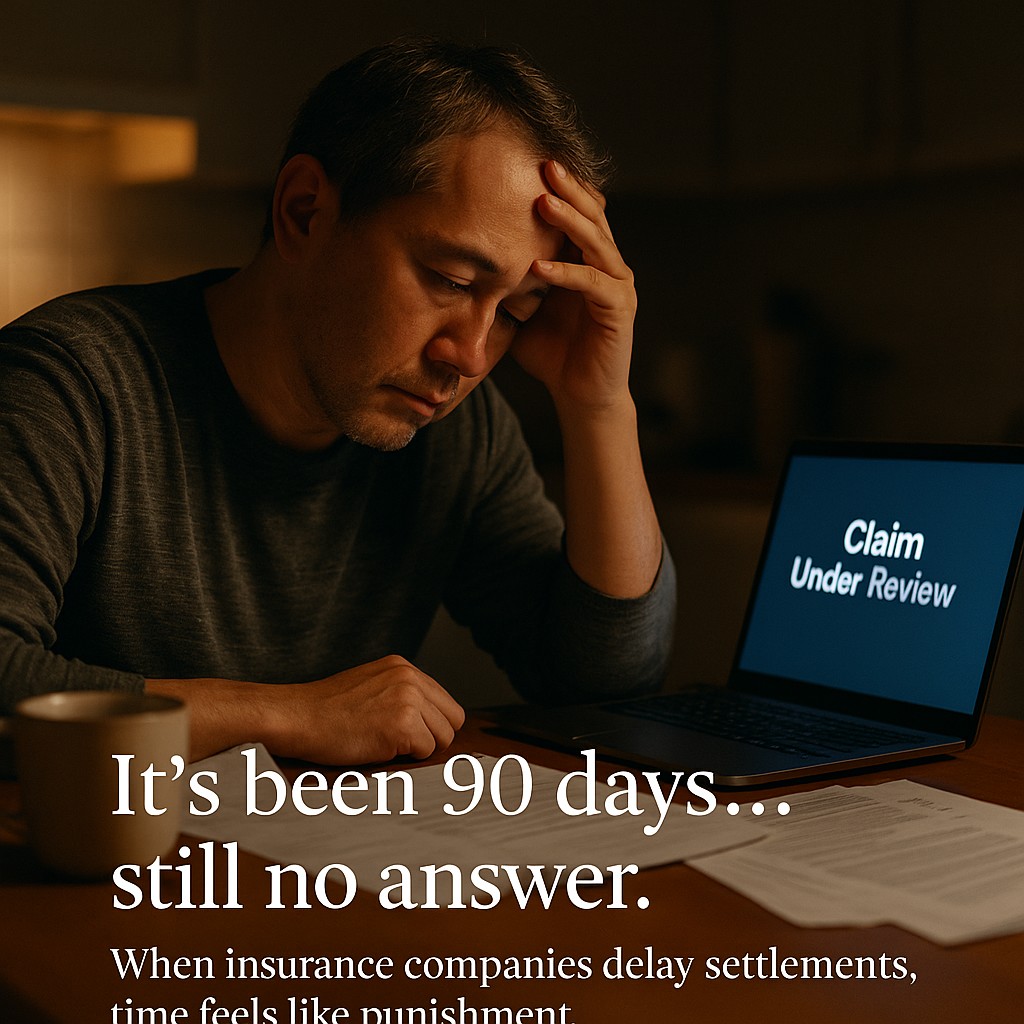

The morning after my exam, I expected progress. Instead, my inbox was quiet. Days became weeks, then months, and I realized this wasn’t a glitch — it was a pattern.

When insurance companies delay settlements, they don’t always say “no.” They simply slow everything until you accept less.

If your medical examination insurance claim feels stuck, this guide explains the hidden incentives, realistic timelines, and the exact steps that help you regain leverage without burning out.

1) The Core Incentive: Why insurance companies delay settlements

Here’s the uncomfortable truth: time is money, and unpaid money earns interest — for the insurer. By stretching the process,

insurance companies delay settlements to reduce immediate payout pressure and nudge claimants toward quicker, smaller agreements.

Internally, delays create opportunities to request clarifications, order re-exams, or send “we need another committee review” messages that sound reasonable but quietly reset clocks.

What a Claims Lawyer Told Me

“Delays are negotiation tools. The longer you wait, the more likely you are to trade dollars for certainty.”

Once you understand that insurance companies delay settlements to change your psychology — not just your paperwork —

you’ll write better emails, set better deadlines, and track every missed commitment in writing.

2) After-Exam Bottlenecks: Where the Clock Quietly Resets

Medical exams anchor your damages, but they also open doors for delay:

- “Clarification” Loops: Adjusters request minor addenda to the report. Each addendum restarts internal review.

- IME/Second Opinion: An insurer-ordered exam can introduce conflicting conclusions — and months of “reconciliation.”

- Committee Calendars: Multi-person signoffs provide plausible reasons to push your file to the next meeting cycle.

- Documentation Drift: If your records aren’t date-stamped, indexed, and complete, you hand them a built-in excuse.

None of this means bad faith automatically — but when insurance companies delay settlements after exams,

these exact points are the gears that quietly turn.

3) Realistic Timeline: From Exam to Offer (and Where Delays Hide)

| Stage | Usual Duration | Common Delay Tactic |

|---|---|---|

| Medical Report Received | 1–2 weeks | “Awaiting attachments”/addenda |

| Adjuster Review | 2–5 weeks | Queue backlog |

| Committee Signoff | 2–4 weeks | Meeting cycles |

| Initial Offer | 1–3 weeks | Low anchor, slow counter |

If your claim passes 90 days with little movement, assume the delay is now strategic. Remember: when

insurance companies delay settlements, they change your expectations first — then your number.

4) Documentation That Speeds Things Up (and Survives Scrutiny)

- Chronological Index: A one-page index of every record with dates, provider, and one-line summary.

- Delta Sheet: A short table of what changed since the last submission (new pain scores, treatments, bills).

- Written Follow-Ups: Email every 14 days with claim ID, unanswered items, and the next decision date you expect.

- IME Counterplan: If they request an IME, ask for the examiner’s specialty, scope, and delivery deadline in writing.

Adjusters move faster when you give them less room to wander. The more your file reads like a finished report, the fewer places

insurance companies delay settlements can stick.

5) Negotiation Without Burnout: Boundaries, Deadlines, Escalation

Negotiation is not a sprint; it’s a schedule. Decide in advance:

- Your Floor: The minimum you’ll accept and why (itemized costs + non-economic rationale).

- Your Clock: The date you’ll escalate if the file sits. Escalation can mean supervisor review or counsel.

- Your Paper Trail: Every promise and deadline in writing. Phone calls are for rapport; email is for records.

When insurance companies delay settlements, they’re testing whether you’ll trade value for relief.

Boundaries keep you from negotiating against yourself.

6) Signs the Delay Is No Longer “Normal”

- Repetitive requests for the same documents after you’ve confirmed receipt.

- IME findings that ignore treating physician notes without explanation.

- Shifting reasons for the hold (“we’re waiting on X” becomes “now we need Y”).

- Silence beyond stated internal timelines with no new date given.

At this stage, assume the incentives are set. The question isn’t whether insurance companies delay settlements —

it’s how you’ll respond, on paper, with a deadline.

7) Email Templates You Can Copy (14-Day Cadence)

Template A — Status + Next Action

Subject: Claim #[ID] — Written Status Update Request (Medical Exam Completed) Hello [Adjuster Name], I’m requesting a written status update on Claim #[ID]. The medical examination was completed on [date]. Please confirm (1) what remains outstanding, (2) the specific decision-maker, and (3) the date you expect the next decision. Thank you, [Your Name]

Template B — Deadline + Escalation Notice

Subject: Claim #[ID] — Timeline Confirmation and Escalation Path Hello [Adjuster Name], To keep our file moving, please confirm the written decision date for Claim #[ID]. If we don’t receive a decision by [date], I’ll request supervisor review so we can finalize this efficiently. Best, [Your Name]

8) When to Consider Counsel

You don’t need a lawyer to send organized emails. But if 90+ days pass with circular answers, counsel adds structure:

demand letters with itemized damages, IME rebuttals from matching specialists, and a litigation clock insurers can’t ignore.

Even then, many cases settle pre-suit once it’s clear that insurance companies delay settlements won’t outlast your documentation.

Insurance Information Institute — Claims Process Guide

A reliable overview of claim stages, internal reviews, and what slows them down.

9) Today’s Takeaway — Your Pace Is Power

When insurance companies delay settlements after medical examinations, it’s rarely about missing files;

it’s about shifting leverage. Your job isn’t to wait — it’s to document, calendar, and escalate.

Clarity beats urgency. Paper beats memory. Deadlines beat drift.